Charts for the Week

Please Note: The charts are for informational purposes only. The information in the charts is believed to be accurate at the time of publication. However, no guarantees are made regarding its completeness or accuracy, and the information may have changed since the time of publication. Readers should not consider the charts as personalized advice or a substitute for professional guidance and should not base any investment, financial, tax, estate, or legal decisions solely on its content.

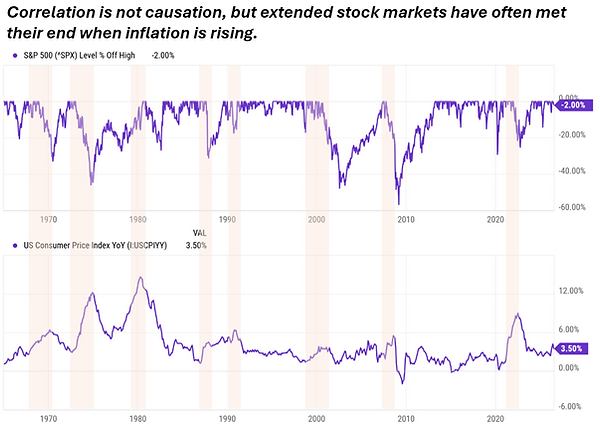

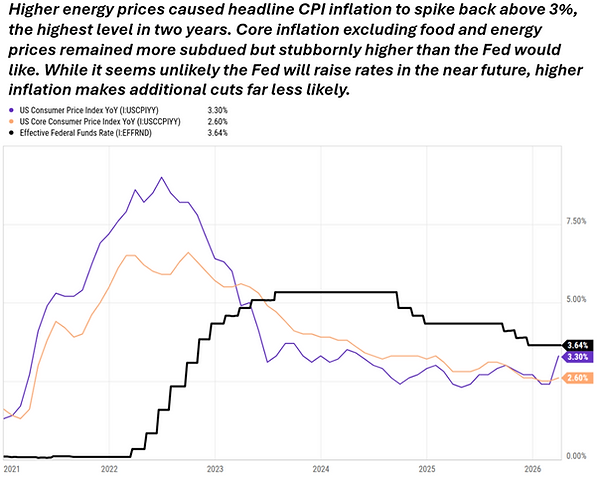

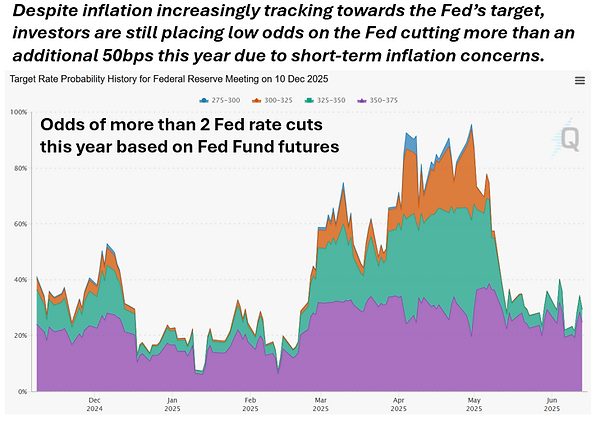

The Fed | Keeps promising low inflation

August 3, 2026

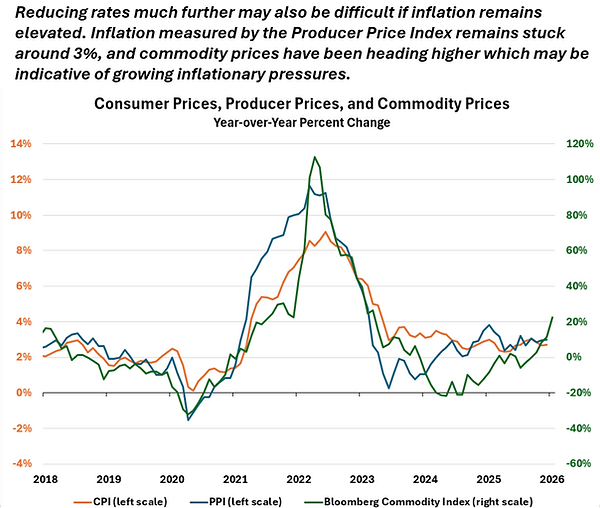

Kevin Warsh held his second policy meeting as Fed Chair, leaning heavily on the Fed’s institutional credibility to keep inflation expectations in check. Policymakers kept the fed funds rate unchanged despite a growing number of dissenting votes in favor of raising rates. By many metrics, the Fed appears to once again be falling behind the curve by keeping monetary policy too accommodative as inflation rises.

Warsh is eager to know what Mr. Market thinks, and not encouragingly long-term interest rates headed higher after the Fed’s meeting with the 30-year Treasury yield reaching its highest level in 19 years, and the stock market was momentarily rattled; however, investors still seem to be giving Warsh and the Fed the benefit of the doubt that they will indeed live up to their often repeated commitment to bring inflation back down to 2%. The stock market quickly righted itself, and market indicators of inflation expectations remain very well anchored to the Fed’s inflation target.

Nevertheless, such confidence in the Fed is unusual in an age of little faith in institutions – especially given its spotty record over the past five years. Low unemployment, steady GDP growth, and a booming stock market certainly make it easier for investors to hold on to the hope that low inflation will be soon re-established.

Despite providing Warsh a grace period to start, Mr. Market has made it clear that tighter monetary policy is expected in the coming year. If inflation stays high and the fed funds rate unchanged through the end of the year, it will become more difficult for investors to believe that the past five years were the anomaly.

Source: YCharts ; https://fred.stlouisfed.org/ ; AOWM Calculations

Travel Indicators | Planes, trains and automobiles

July 27, 2026

Vacation spending is one of the largest discretionary consumer expenses. Accordingly travel trends can provide insight into the overall health of the economy. Like much of the economic data these days, the picture is muddled but is also not raising any clear red flags.

Overall spending on travel and transportation services is growing steadily and not exhibiting any weakness that might be an early warning sign for the broader economy. That said, air travel has flatlined while the railroads have gotten busier which may be indicative of the now infamous k-shaped economy where the top-end of the economic ladder is doing well while everyone else is pinching pennies.

Surveys continue to report that the consumer feels depressed – perhaps all the more reason to splurge on an escape from the daily grind.

Source: YCharts ; https://fred.stlouisfed.org/ ; https://www.ustravel.org/research/travel-forecasts ; https://data.bts.gov/stories/s/Transportation-as-an-Economic-Indicator-Seasonally/j32x-7fku ; AOWM Calculations

Inflation | Still worrisome

July 20, 2026

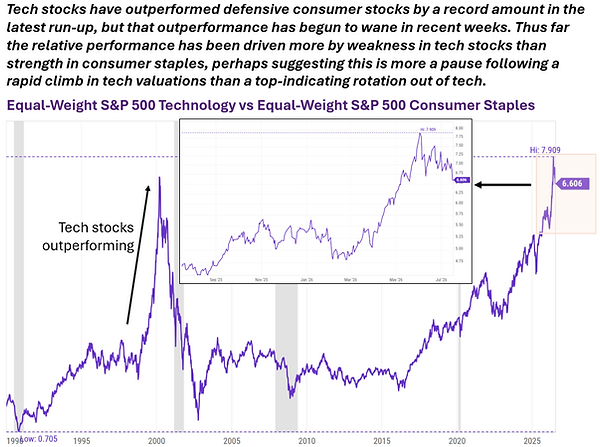

Rabid bull markets running wildly from the historical mean do not like to see rising inflation. Whether it is the tighter monetary policy that usually accompanies accelerating inflation or the psychological cold water poured on sentiment by higher consumer prices or the erosion of profit margins or just pure historical coincidence when everthing is running too hot, prolonged downturns in the stock market often take root when inflation is spiking.

In that regard, the June CPI report that showed a rapid deceleration in inflation should have been very welcome news. Unfortunately, the falling energy prices that helped to lead inflation lower last month have already started to head higher again as the conflict with Iran has reignited. As a result, investors’ expectations for the Fed to raise rates barely changed despite inflation coming in well below expectations.

While the recent weakness in tech stocks and the outperformance of boring old economy stocks likely has nothing to do with concerns about inflation or monetary policy, bulls with long memories may still be nervously twitching at the prospect of an amplifying wave of inflation.

Source: YCharts ; https://fred.stlouisfed.org/ ; https://econforecasting.com/forecast/ffr ; AOWM Calculations

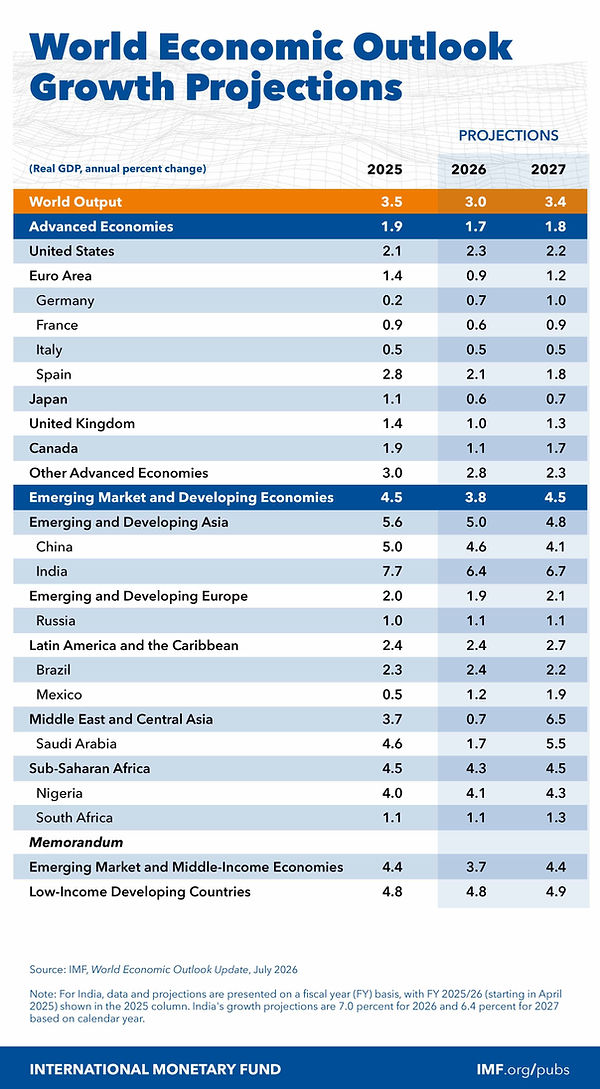

Economic Outlook | Just right

July 13, 2026

The ideal economic backdrop for the financial markets is steady growth and low inflation, and that is exactly what investors appear to be anticipating at the moment. In the TIPS market, in particular, real interest rates have been rising (suggesting solid economic growth) and expected inflation has been falling (implying confidence low inflation will be re-established before long).

The fact that asset valuations have surged so high despite five years of problematic inflation is a testament to the power of a new transformative technology to capture investors’ imaginations. It also doesn’t hurt that it is easier than ever to gamble in the financial markets while government stimulus has well exceeded any other time of general peace and prosperity – and appears to be becoming more stimulative once again.

Given that the recent past is often the best prediction of the near future, the low inflation outlook may be optimistic, but that may not be enough to disrupt the market mania just yet.

Source: YCharts ; https://fred.stlouisfed.org/ ; Factset ; IMF.org ; AOWM Calculations

Labor Market | Mid-year check-up

July 6, 2026

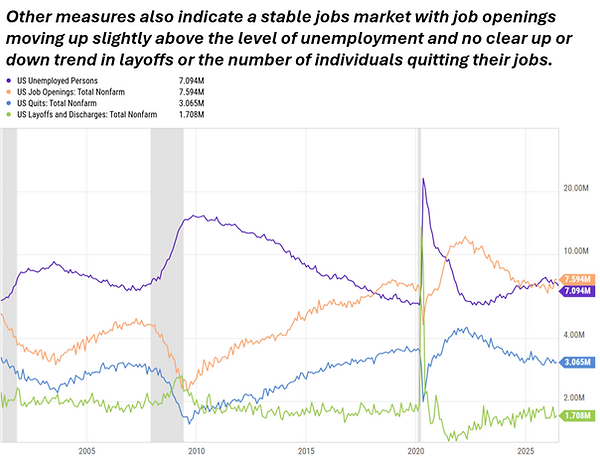

The vital signs for the labor market remained stable in June. Payroll growth was weak and previous months’ data were revised lower, but the trend this year is still positive, and the unemployment rate remains low. Job openings have also ticked back above the unemployment level while the number of individuals quitting or being laid off are both little changed over the past 18 months.

And yet the jobs market’s health is far from as robust as one would expect given the steady pace of economic growth and booming financial markets. Sources of strength remain concentrated in a few sectors, annual payroll growth continues to be anemic, the participation rate and the size of the labor force are contracting, and average wage growth is once again lagging inflation.

Aging demographics and potential AI disruptions make it more challenging to gauge how the labor market is really doing. However, overall, policymakers likely remain generally comfortable with its health at the moment.

Source: YCharts ; https://fred.stlouisfed.org/ ; AOWM Calculations

Earnings Expectations | Extreme optimism

June 29, 2026

As the second quarter draws to a close, earnings growth remains robust, and expectations for future profits are increasing even faster. Rising consensus estimates for companies in the S&P 500 are now projecting earnings for the quarter to once again be up more than 20% compared to last year. The good times are anticipated to keep rolling for as far as the eye can see with long-term earnings growth expectations at all-time highs.

Decades of expanding profit margins and the transformational nature of AI are amplifying investors’ tendency to project the current moment well into the future. However, such extreme optimism has historically been an ominous omen for the market.

The outlook relies in no small part on massive AI capex spending continuing to accelerate higher, but the languishing stock prices of the AI hyperscalers suggests there may be emerging doubts about that – or about the return those hyperscalers are likely to reap if they continue spending ever more on data centers.

Source: YCharts ; https://fred.stlouisfed.org/ ; Topdowncharts.com ; JPMorgan ; www.gurufocus.com ; AOWM Calculations

The Fed | Regime change?

June 22, 2026

Kevin Warsh kicked off his tenure as Chair of the Federal Reserve with an initial attempt to roll back the clock to a time when monetary policy was simpler and more mysterious. The policy statement was chopped down to 130 words from 341 in the previous statement, and Warsh declined to provide his own forecasts for the economy, inflation or the Fed funds rate. However, monetary policy is still run by committee, and other policymakers provided projections that indicated a transitory concern about inflation and a likely need to keep the Fed funds rate where it is if not even potentially a tick higher.

Warsh dodged answering many questions during his press conference by pointing to the numerous task forces he has initiated to review every aspect of the how the Fed implements monetary policy. He even equivocated on whether he viewed current Fed policy as being restrictive or accommodating, suggesting it is perhaps a bit of both depending on the sector. Given that a dovish outlook helped him get nominated, that was not a terribly surprising evasion.

Warsh did at least basically acknowledge the undeniable fact that the financial markets are more than a little juiced at the moment. He also indicated that he would like policymakers to pay more attention to what the financial markets are telling them. That would be a refreshing change but would lead to a less equivocal view of where the Fed currently stands.

Source: YCharts ; https://fred.stlouisfed.org/ ; https://www.census.gov/construction/c30/c30index.html ; AOWM Calculations

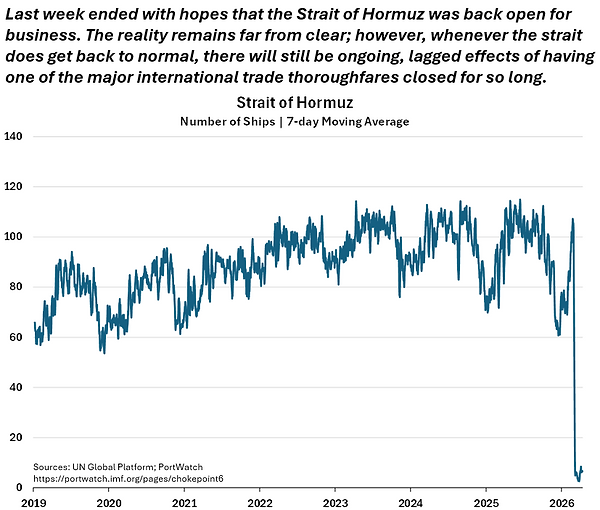

Inflation | Surely transitory

June 15, 2026

Last week offered more bad headline inflation reports for consumer prices and producer prices. Surging energy prices pushed both the annual inflation for the CPI and PPI to their highest levels in over three years. Core inflation, excluding energy and food prices, was less alarming but is still trending in the wrong direction.

For those eager to see the Fed loosen monetary policy, the increase in inflation is effectively doing that without the Fed having to do anything. And the market continues to expect the central bank to do nothing at least for the next several months. The announcement of a potential deal to reopen the Strait of Hormuz will make it easy for policymakers to kick the can down the road in the hope that oil prices and inflation will decline over the coming months.

Like investors, policymakers have grown increasingly comfortable operating without a margin for safety since nothing really bad ever happens.

Source: YCharts ; https://fred.stlouisfed.org/ ; AOWM Calculations

Good News | Bad news

June 8, 2026

It took a positive jobs report to break the stock market’s nine-week winning streak. Initial estimates for payroll growth indicate the economy has generated three straight months of solid gains, and the unemployment rate remained low at 4.3%. The good news increased the odds the Fed will increase short-term interest rates this year to combat rising inflation.

Whatever the news, the stock market was overdue for a selloff after its recent run. And, beyond higher interest rates, there are a few other things going on in the world that could have reasonably given investors pause or triggered selling pressures. As the juggernaut that is the stock market rolls towards the largest IPO in history this week, there are signs of potentially waning risk appetites in other asset classes, such as crypto currencies and gold which are both well off their highs.

Nevertheless, despite concerns about tighter monetary policy, good economic news is better than the alternative when trying to launch mega IPOs into space.

Source: YCharts ; https://fred.stlouisfed.org/ ; BLS ; https://taxtracking.com/post3/ ; AOWM Calculations

Stocks | Sell in May...

June 1, 2026

The S&P 500 is on a nine-week winning streak for only the fifth time since 1965. After such a run and with the market at historically elevated valuations, the adage to “sell in May and go away” may seem to hold more wisdom than usual. However, the summer months have actually been the market’s best in recent years, and who knows how high the market can fly.

Despite economic growth for the first quarter being revised lower, stocks still enjoy the tailwinds of a steadily expanding economy, booming corporate profits, and a powerful AI cap ex super cycle. Those good fundamentals are being valued very richly, even while reports last week of rising inflation and falling savings suggest there are reasons to be cautious about the sustainability of those market tailwinds.

Investor sentiment is incessantly swinging from one extreme to another, and the pendulum has swung to the point where old wisdom appears foolish in many respects.

Source: YCharts ; https://fred.stlouisfed.org/ ; AOWM Calculations

Fed Chair #17 | Godspeed

May 25, 2026

Kevin Warsh was sworn in as the 17th Fed Chair last week at a moment of discombobulating technological change, booming financial markets, and growing systemic risks. The economy is growing (but the drivers of growth are not broad based); unemployment is low (but job growth is stagnant); asset prices keep going up (but valuations are stretched and the stock market is highly concentrated). Inflation is also rising again; thus, investors have started to price in Fed rate increases later this year which could put Warsh in an awkward spot right out of the gates.

More challenging for Warsh and the Fed than failing to deliver lower rates is the increasing fragility of the system. High valuations on their own are an indicator of increasing risk, but the potential trouble is amplified when coupled with record leverage via options and margin loans. With the federal debt trending past 100% of GDP and the real fed funds rate already accommodative, government policy is poorly positioned for any downturn with additional stimulus potentially creating as many problems as it solves. National savings is unsustainably low, inflating corporate profits that are being further inflated by an unsustainable AI capex cycle. And, if they succeed in getting issued at their advertised trillion plus dollar valuations, the coming mega-cap IPOs would check the box for what has been a missing sign of an overwrought market and bring uncertain systemic consequences given their unprecedented size.

Trying to predict how crazy things will get is a maddening exercise. However, the crowd has long since slipped into viewing not just predictions as worthless, but preparation as well - not just plans, but also planning. The sun is shining, but no attention is being paid to the roof riddled with holes. Godspeed to the new chief lender of last resort when the rain comes.

Source: YCharts ; https://fred.stlouisfed.org/ ; https://econforecasting.com/forecast/ffr ; https://site.warrington.ufl.edu/ritter/files/IPO-Statistics.pdf ; AOWM Calculations

Inflation | Round 2

May 18, 2026

A global energy shock is pushing inflation higher, and bond markets around the world are starting to take notice. Long-term interest rates spiked higher at the end of last week, reaching a level that may even start to draw the attention of equity investors impervious to danger. Or not -- after all, the stock market largely brushed off the surge in inflation five years ago during the pandemic boom and only took a brief pause in 2022 when the Fed finally embarked on normalizing monetary policy from a wildly accommodative position before the AI run-up commenced.

This go round, the Fed is again unlikely to rush into action. Kevin Warsh, the incoming Fed Chair taking the helm this week, confronts the challenge of spiking inflation and a profligate federal government craving lower interest rates to help finance its spending. His answer to the conundrum may be to try convincing his new colleagues to resume shrinking the Fed’s balance sheet to combat inflation but leave its target overnight interest rate unchanged.

Like much of monetary policy over the past two decades, it would be a live experiment to see if inflation can be completely brought to heel without a full monetary tightening (and/or an economic downturn).

Source: YCharts ; https://fred.stlouisfed.org/ ; https://streetstats.finance/rates/tips ; AOWM Calculations

Investors | Pole vaulting the wall of worry

May 11, 2026

Risks are increasing, but investors seem increasingly confident they will never materialize. The AI boom is pole vaulting the wall of worry.

The S&P 500 is on a six-week winning streak and continues to post record highs while consumer sentiment continues to post record lows. The Strait of Hormuz remains closed, but everyone assumes it will be opened before the decline in oil supplies causes a heart attack for the global economy. Job growth remains stagnant, but the low unemployment rate provides comfort that this is the new normal and not the harbinger of an economic slowdown. The federal government debt is trending past 100% of GDP and inflation is ticking higher, but the markets register minimal investor concern.

Barring an actual economic disruption (not just the growing risk of one) that alters increasingly optimistic earnings forecasts, the market’s momentum seems determined to increase valuations to ever riskier heights balanced on the needle of AI hopes and dreams.

Source: YCharts ; https://fred.stlouisfed.org/ ; shillerdata.com ; AOWM Calculations

Corporate Profts | Another k-shaped anomaly

May 4, 2026

The economy continued to expand at a steady pace in the first quarter, but corporate profits are exploding higher. With nearly two-thirds of the companies in the S&P 500 having reported Q1 results, earnings per share for the index are on track to be up nearly 30% from last year. It is yet another k-shaped historical anomaly for profit growth to be accelerating when economic growth is decelerating.

The AI investment boom has created a virtuous flywheel for corporate America with high profits for AI hyperscalers enabling ever larger capital expenditures which boost the profits of other companies in the data center food chain fostering more AI enthusiasm that pushes up stock valuations which boosts general consumer spending via a robust wealth effect that feeds more corporate profits.

If the hyperscaling investments in AI do not generate sufficient returns, current reported profits will ultimately prove to have been overstated, and the hangover could be rough as the flywheel goes in reverse. Even if all the AI cap ex proves to have been wisely spent and continues to ramp higher as expected, long-run returns for investors from current elevated stock valuations are still likely to be meager.

Source: YCharts ; https://fred.stlouisfed.org/ ; shillerdata.com ; AOWM Calculations

Old Oil | Going to ruin the party?

April 27, 2026

The stocks of semiconductor companies have ripped higher in recent weeks as the AI trade has roared back to life. The PHLX Semiconductor Index has had a record 18 straight positive trading days and is up nearly 50% since March 30.

Semiconductors have been called the new oil of the 21st century – the essential resource powering the digital age and especially the AI revolution. Based on projections for what it will take for artificial intelligence to achieve its potential, anything associated with the necessary data center buildout has had been bid up to levels that appear illogical even based on the most optimistic forecasts. Regardless of logic, the party seems likely to go on as long as companies are flush with profits and spending increasing amounts on AI and its development.

However, the essential resource of the 20th century may spitefully remind the world it is still important. While we are less dependent on fossil fuels than in the past, supply disruptions still leave a mark on the economy. While continuing to await a diplomatic breakthrough to reopen the Strait of Hormuz, investors seem oddly at ease about the growing oil shock moving towards the economy – albeit at the glacial pace of a tanker.

Source: YCharts ; https://fred.stlouisfed.org/ ; AOWM Calculations

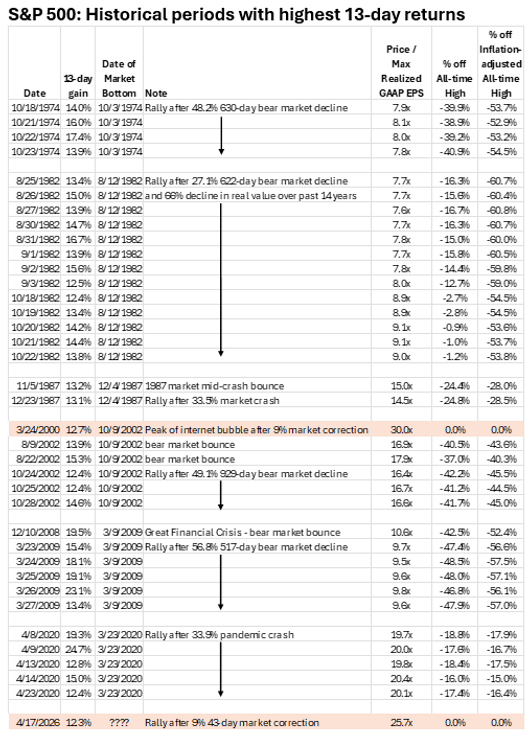

Momentum Thrust | Jumping the shark

April 20, 2026

The two-week ceasefire in Iran generated a rally in stocks that has only been seen a handful of times over the past seven decades. Even without a peace deal or the resumption of trade through the Strait of Hormuz, investors have seized on any hints that the Iran war can be quickly filed away as just another geopolitical disturbance of little lastly consequence to the financial markets.

Positive early reports for first quarter earnings have reinforced the fast and furious return of bullish investor sentiment. Expected earnings for the S&P 500 continue to head higher with analysts now projecting 18% earnings growth this year. Robust forecasts for corporate profits are a powerful tailwind for the market; however, forecasts can change quickly, and the lagged effects of the turmoil in the Middle East may yet upset rosy outlooks even if the current situation is soon brought to a close.

In addition, some market behavior this past week had the late stage feeling of the Fonz jumping over a shark. While such a strong rally over such a short period has historically been a good sign for future returns, that is because it has typically occurred after a prolonged, deep bear market. The only other time a 13-day rally of more than 12% has ended at an all-time high was the absolute peak of the internet bubble in 2000 – a historical analogue at least worth a moment of pause.

Source: YCharts ; https://fred.stlouisfed.org/ ; https://portwatch.imf.org/pages/chokepoint6 ; AOWM Calculations

Wonderland | Curiouser and curiouser

April 13, 2026

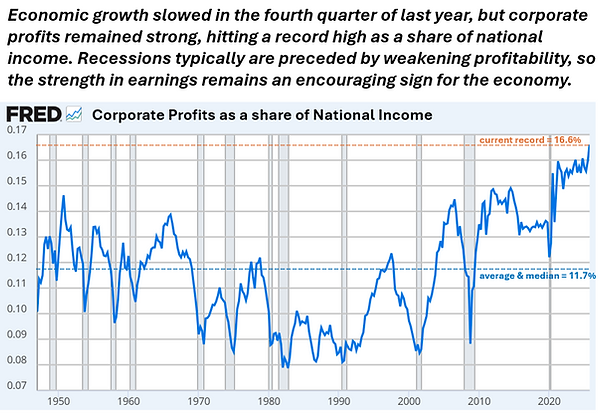

Since the pandemic, we seem to have tumbled down a rabbit hole into an increasingly surreal world where everybody is mad in their own way and believing six impossible things before breakfast is required – a reality well depicted by last week’s economic and market news. While the stock market was surging back to within a whisker of record highs on hopes springing from a ceasefire with Iran, consumer sentiment – as measured by the University of Michigan since the 1950s – hit an all-time low.

The dissonance between how folks say they feel about the economy and the hard economic data has been notable for some time; however, a record low when the stock market is near record highs, unemployment is low and the economy is growing still takes some practice to believe. One culprit for the era of poor feelings is undoubtedly inflation which was reported last week to have spiked back above 3% in March because of rising energy prices – this of course gave neither equity nor fixed income investors much pause.

In investors’ defense, last week also saw it reported that corporate profits had hit a record high as a share of national income at the end of last year. While clearly welcome news for shareholders, it is also a reassuring sign for the economy as recessions have usually been preceded by weakening profitability of which there are no signs. That said, once upon a time, declining consumer sentiment was a good leading indicator of consumer spending, but that was before consumers grew accustomed to swimming in their tears.

Source: YCharts ; https://fred.stlouisfed.org/ ; https://data.sca.isr.umich.edu/ ; shillerdata.com ; AOWM Calculations

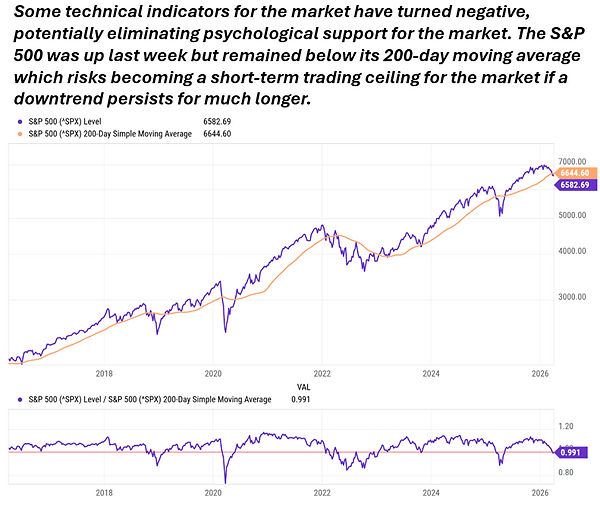

Investor Sentiment | Losing technical support

April 6, 2026

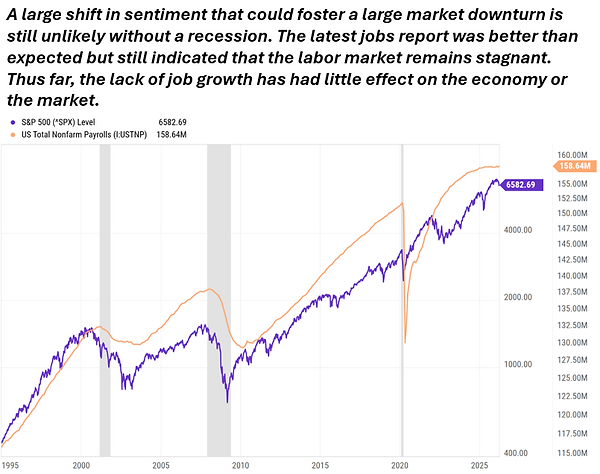

The S&P 500 broke its losing streak last week. Investors appear to be largely keeping the faith that this time will not be different - the market and the economy have been resilient in the face of countless worries in recent years and will be again. The jobs report for March released last week was certainly better than feared and provided support for the case that the economy will motor through the disruptions to the energy markets.

Without a recession, sentiment seems unlikely to sour sufficiently to lead to a large market downturn. While anxiety has been inching higher, investors entered the year at peak levels of optimism as measured by their allocation to stocks. The danger from such heights is that any downshift snowballs into a self-fulfilling reality, especially for an economy that has ridden the tailwind of a large wealth effect.

With some technical market indicators turning negative in recent weeks, investors’ past extreme confidence may offer little support and could prove to be wax wings.

Source: YCharts ; https://fred.stlouisfed.org/ ; AOWM Calculations

Animal Spirits | Chastened

March 30, 2026

The S&P 500 is on a five-week losing streak and has registered just three positive weeks so far this year. Even the high-flying tech sector has fallen into correction territory, ending last week 13% off its recent all-time high. The fear that higher energy prices could push the economy into a recession accompanied by rising inflation has chastened investors’ animal spirits.

Of course, the exact same fear haunted the market in 2022, and those fears proved unwarranted as the highly anticipated recession never arrived. At that time, the arrival of AI, declining inflation, and a new surge of fiscal stimulus revived the economy and the market’s upward momentum after what in hindsight was just another brief correction in the epic bull market of the past seventeen years.

This may turn out to be merely another bump in the march to an even wilder top. However, the geopolitical environment feels even more unpredictable than usual, inflation is ticking higher, AI has become a juggernaut that seems intent on destroying as much market value as it creates, and both monetary and fiscal policy are increasingly constrained in their ability to bail out the economy. Accordingly, investors are pushing the pause button on paying top dollar for highly optimistic expectations – at least for the moment.

Source: YCharts ; https://fred.stlouisfed.org/ ; https://insight.factset.com/ ; www.richmondfed.org/research/national_economy/cfo_survey ; AOWM Calculations

The Fed | On hold again

March 23, 2026

For the second year in a row, the Fed is entering a holding pattern after a series of year-end rate cuts. This time the prospects for additional reductions in the Fed’s short-term target interest rate seem lower than they have at any point over the past couple years of easing monetary policy. Indeed, investors have started to price in the possibility that the Fed will have to raise rates in response to higher inflation fueled by the disruptions in the energy markets.

Despite shaky financial markets highlighting concerns that rising oil and gas prices could push the resilient US economy into a recession while simultaneously sending inflation higher, the Fed is not yet stuck in a stagflation quagmire, nor are policymakers anticipating such a challenging environment.

The Fed’s quarterly update of economic projections shows that our central bankers are still expecting inflation to decline this year (though less than previously forecasted). In addition to a relatively benign inflation forecast given the state of the world, Fed officials also boosted their estimates for GDP growth in both their short-term and long-term outlooks. It is an optimistic outlook – one that Mr. Market generally shares, albeit more nervously at the moment.

Source: YCharts ; https://fred.stlouisfed.org/ ; https://kalshi.com/ ; Federal Reserve ; AOWM Calculations

Investors | Expecting less help from the Fed

March 16, 2026

Estimates for GDP growth in the fourth quarter of last year were revised significantly lower, but market expectations for additional monetary easing this year are also being revised down. Investors are now anticipating just one quarter percentage point reduction in the Fed’s target overnight rate sometime later this year as concerns about inflation outweigh worries about economic growth.

Inflation was already showing troubling signs of trending in the wrong direction before the latest conflict in Iran sent oil prices higher. Despite long-term rates and inflation expectations moving up, investors appear to still have faith that the Fed will not let inflation become a long-term problem even if it means providing less support to the economy in the short run.

The stock market remains wobbly as weaker economic growth and higher inflation are an unwelcome combination. But thus far, the recent sell-off remains well within the bounds of normal volatility from which a short-term bounce higher would also not be unusual. That would provide more comfort if the market wasn’t still perched so precariously high at a time such as this.

Source: YCharts ; https://fred.stlouisfed.org/ ; US BEA; https://www.cmegroup.com/ ; AOWM Calculations

Spiking Oil Prices | An ominous omen

March 9, 2026

Geopolitical uncertainty is slowly starting to affect financial markets. The “fear index” of expected volatility has spiked higher, and the S&P 500 is losing altitude. Nevertheless, all things considered, the stock market has held in relatively well and remains close to its all-time high as investors have been trained to brush off world events as unlikely to have more than a fleeting effect on stock prices. The ongoing spike in oil prices may change that calculus, especially if it persists for any length of time.

Rising oil prices have frequently led or coincided with economic and market downturns, and the current disruption occurs at a time when the economy is slowing, and asset valuations remain highly susceptible to revaluation.

Investors may take comfort in the Administration’s past ability to quickly reignite the market's animal spirits after periods of heightened uncertainty. A fast resolution of the Iranian conflict may do that again, even potentially giving the stock market renewed momentum towards fresh all-time highs. However, if the powers-that-be fail to deliver, the lost perception of control over the financial whirlwind could worsen the downside tail risk.

Source: YCharts ; https://fred.stlouisfed.org/ ; AOWM Calculations

The Market | Priced for perfection

March 2, 2026

Current market valuations leave little margin for error. In an unsettled world with geopolitical turmoil and revolutionary technological changes happening at seemingly warp speed, the risk of things not going perfectly should give investors some pause, and it may be beginning to do so.

Investors have climbed a wild wall of worry in recent years. With each avoided catastrophe, risk appetites have grown larger. Potential negative outcomes may continue to be avoided, but the pain of any misstep grows with fearless confidence. Certainly, the long-run trend for the market is upward, and any investment in equities is a bet on the future being brighter than today – which has historically been a good bet. And yet, the premium return offered for investing in equities exists precisely because the future is not certain. Pricing stocks as if tomorrow’s outcome is guaranteed (and then some) can lead to years in the wilderness relearning that lesson before resuming the upward march.

The rotations happening recently underneath the placid surface of the headline market index suggest that investors may be starting to question the high valuations of the mega cap stocks. A lengthy, calm sideways march for the market overall would be a disappointment for investors who have grown accustomed to double-digit returns, but it would be another worry avoided for the economy.

Source: YCharts ; https://fred.stlouisfed.org/ ; shillerdata.com ; AOWM Calculations

The Economy | How different is this time?

February 23, 2026

The economy slowed at the end of last year even as the Fed’s preferred PCE inflation metric accelerated back towards 3%. While GDP growth was weak in the fourth quarter at least partly because of the lengthy government shutdown, the economy still posted solid growth above 2% for the full year and is widely expected to keep chugging along steadily at that pace.

The lack of growth in the labor market would typically raise a few alarm bells about the economy, but demographics and AI offer potential explanatory stories as to why this time is different. And yet the current macro picture is not that dissimilar from other periods leading into a downturn – with the stock market perhaps being the true exception. Rarely has the stock market been hovering near all-time highs when job growth has completely stalled.

That could be an encouraging sign that this time really is different for various reasons. Or it could be a discouraging omen that the economy has already weakened so much while the wealth effect from a record stock market is still so strong. But if the economy is teetering perilously, the Supreme Court may have added an extra stimulative boost last week in the way of potential tariff refunds to go with all the government stimulus that is already in the pipeline for this year (which is perhaps why investors remain generally sanguine).

The real trouble may start if or when government stimulus is no longer seen as a positive, especially with respect to inflation.

Source: YCharts ; https://fred.stlouisfed.org/ ; https://americanstaffing.net/research/asa-data-dashboard/gdp-quarterly-projections/ ; AOWM Calculations

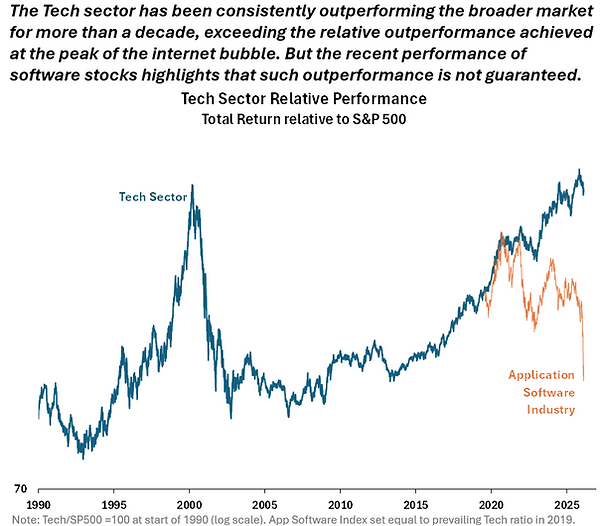

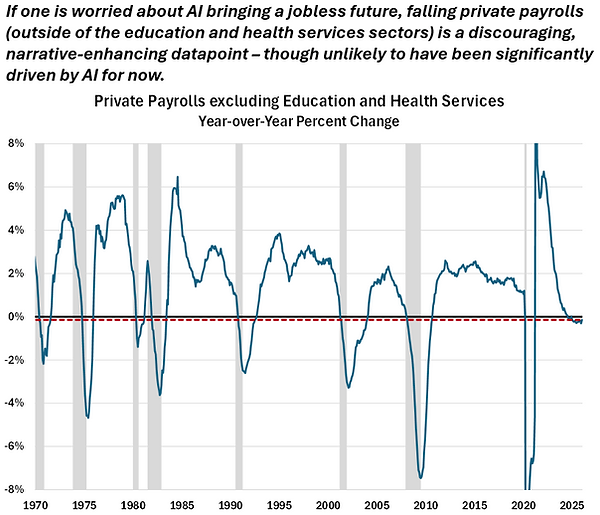

AI | The unknown, inevitable future

February 16, 2026

Technology bubbles thrive on an uncertain future which allows imaginative narratives to be spun about what is to come and the riches to be had. Such stories can make the future feel inevitable; although not always in a good way, as investors in software companies have learned in recent months. Even the stocks of the hyperscalers racing to own the future have come under pressure as the AI revolution is starting to feel even more discombobulating than past technological leaps with a potential end that is far from glorious.

And yet, the AI juggernaut seems unstoppable and continues to at least boost the stocks of those offering the picks and shovels for building datacenters. Given the speed at which AI is purportedly moving, the cloud of uncertainty around what it will truly bring may lift sooner rather than later – which will at least provide relief from the exhausting hype.

For now, recent macro-economic data has provided narrative-enhancing datapoints that we are headed towards a jobless, low-inflation future (even if AI is unlikely to have had much to do with either up to this point). Nevertheless, the combination of falling inflation, low unemployment, zero job growth, and solid GDP growth reinforces that we are living in unusual times.

Source: YCharts ; https://fred.stlouisfed.org/ ; JP Morgan ; AOWM Calculations

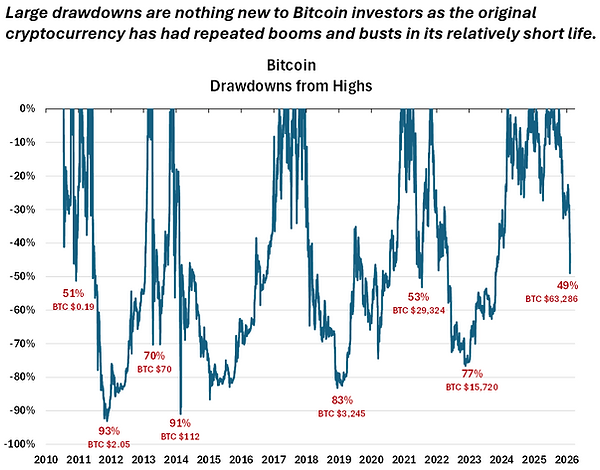

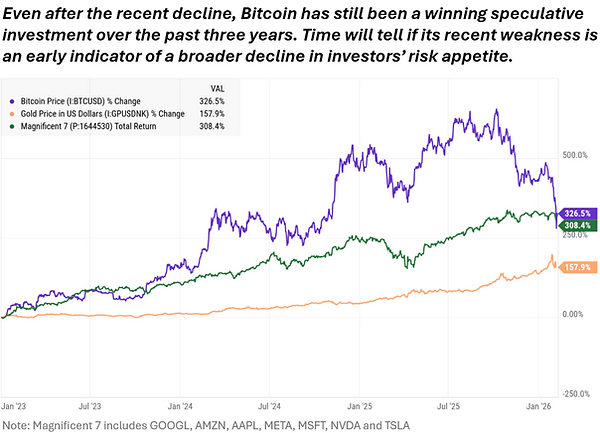

Crypto | Rumors of the end swirling again

February 9, 2026

Many of the hot investments of the past few years have lost some of their luster in recent months. In particular, cryptocurrencies have experienced a large decline, losing over $2 trillion in market value since October before recovering slightly in recent days. At the low point last week, Bitcoin - the original and largest cryptocurrency - was down nearly 50% from its October high.

Such wild swings are nothing new for crypto investors. Bitcoin has had more lives than a fabled cat in its relatively short sixteen years. With each perilous fall, Bitcoin has seemed destined for the dustbin of history; however, each time, the new age gold has risen like a Phoenix to even greater heights.

The precise cause of the recent selloff is impossible to know. Perhaps it has been driven by concerns about the nomination of a new Fed Chair who is less inclined to expand the Fed’s balance sheet. Or perhaps there are growing fears that AI will eventually make cryptos easy to hack and thus worthless. Or there may just be a growing wariness among investors which shows up more quickly in the less liquid crypto markets than elsewhere.

Whatever the cause, the sell-off was unexpected for a newly accepted asset class with many apparent tailwinds – a reminder that in the short-run markets rarely act as anticipated.

Source: YCharts ; https://stooq.com/ ; https://coinmarketcap.com/ ; https://www.tradingview.com/ ; AOWM Calculations

New Fed Chair | Still a majority vote

February 2, 2026

Last week, the President nominated Kevin Warsh to be the next Chair of the Federal Reserve Board after a lengthy search. As a former Fed governor, Warsh is a noncontroversial, conventional pick who is well qualified to be the first among equals on the Fed Board and its monetary policymaking committee. Even with a new Fed Chair, however, the President is still unlikely to get the dramatically lower interest rates he desires.

Warsh has indicated that he favors lower interest rates, but he will have to convince a majority of his Fed colleagues to go along. For now, that seems likely to be a hard sell – at least beyond the two quarter-point rate cuts investors expect later this year (an expectation that was little changed after the announcement of Warsh’s nomination). If inflation remains elevated and headline GDP growth generally strong, even those anticipated cuts may not have majority support at the Fed.

In addition to not being able to deliver radically lower rates, Warsh may end up being less of a friend for the stock market than recent leaders of the Fed have been. In particular, he has been critical of the massive expansion of the Fed’s balance sheet since the 2008 financial crisis and has voiced a desire to see it reduced in size.

The monetary experiment in “quantitative easing” has generally been viewed as a positive for equity valuations – if only for psychological reasons. The markets can be reassured that any responsible taming of the Fed’s balance sheet would take years. Nevertheless, investors may still be disappointed if Warsh can persuade his colleagues that they need not break out the QE firehose to quell every fire.

Source: YCharts ; fred.stlouisfed.org ; newyorkfed.org/research/policy/rstar ; cmegroup.com/markets/interest-rates/cme-fedwatch-tool.htm ; AOWM Calculations

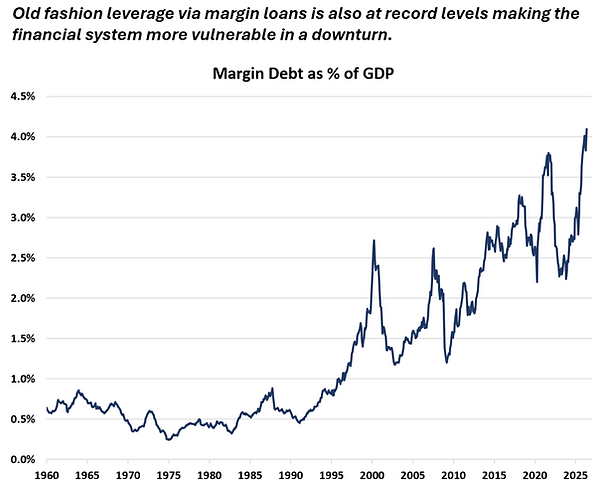

Risk Appetite | Still healthy

January 26, 2026

The financial markets were a little wobbly last week, but investors’ appetite for risk remains robust. Despite shifting tectonic plates that at a minimum increase uncertainty about the future, the prevailing market sentiment reflects Elon Musk’s admonition at Davos that it is better to be optimistic and wrong than pessimistic and right.

While asset valuations, credit spreads, option market activity, and margin debt all indicate that investors may be overindulging in risk, none provide a clear signal for when that might change or result in an upset stomach. If anything, some risk indicators offer reassurance that the bell has yet to be rung at the top.

For investors, optimism currently not only offers a happier outlook on life but appears to provide immeditate rewards as well. However, maintaining a long-run optimism when things go wrong is the challenge that derails the compounding returns of many.

Source: YCharts ; fred.stlouisfed.org ; BoA ; FINRA ; CBOE ; shillerata.com ; AOWM Calculations

The Economy | Two supercharged engines

January 19, 2026

AI investments and wealthy consumers are driving economic growth these days, supercharged by a high level of government stimulus which has made it easier for businesses and individuals to splurge (to a potentially destabilizing degree).

Technology-related private investments have been trending higher for decades as the world has become increasingly run by ones and zeros. However, there was a hangover after the internet bubble, and only with the recent surge in AI spending have such investments surpassed that 2000 peak as a share of the economy. And at the moment, AI investments are responsible for nearly all the growth in private investments with some segments even declining at a disconcerting rate.

To the extent there is any economic weakness, extra monetary and fiscal stimulus is on the way even though the consensus outlook is for continued steady growth. Government policies in recent years have largely eschewed the traditional wisdom of trying to be a ballast for the economy with all parties choosing to run it “hot” – fingers crossed.

Source: YCharts ; fred.stlouisfed.org ; BEA ; CBO ; AOWM Calculations

Economic Growth | Productivity growth dependent

January 12, 2026

The labor market remains an enigma. Payroll growth has ground to a halt, but the unemployment rate fell to 4.4% in December (and November’s unemployment rate was revised lower to 4.5%). Absent the addition of workers, economic growth will be solely dependent on productivity gains.

On that front, the recent data is encouraging with productivity growing at an annualized rate of 4.5% over the second and third quarters of last year. However, those strong gains were on the heels of two very weak quarters, so the longer trend still shows productivity decelerating over the past two years while payroll gains have also slowed - not exactly the advertised roaring 20s from a macro perspective.

Much enthusiasm is riding on AI generating miraculous improvements in efficiency. To date, such a miracle has not materialized in the government statistics. But it is early and the recent data will be revised many times before being deemed final, so the present may look different in the future. Till then, we can gaze back longingly at the late 1990s when the macroeconomic fundamentals at least made a tech bubble seem slightly more rational.

Source: YCharts ; fred.stlouisfed.org ; BLS ; AOWM Calculations

2025 & 2026 | Review & preview

January 5, 2026

Prognosticators were generally optimistic as last year began, and 2025 turned out largely as hoped. The economy slowed but continued to expand steadily. Unemployment ticked higher, but remained low. Inflation moderated slightly but remained stubbornly above the Fed’s 2% target. Interest rates headed lower. And the stock market climbed solidly higher as corporate profits expanded nicely.

The consensus outlook for 2026 is for more of the same: steady growth, low unemployment, falling inflation, declining interest rates, and another good year for the stock market on the back of strong earnings growth. The additional monetary and fiscal stimulus in the pipeline supports expectations for the economy and the markets to have another good year. And when the stock market has been up more than 16% in six of the last seven years, it’s hard not to assume that such high, consistent returns are the norm.

Nevertheless, with every ratchet higher of government stimulus and market valuations to historically extreme levels, caution becomes more warranted and straight-line forecasts more dubious.

Source: YCharts ; fred.stlouisfed.org ; S&P ; https://www.ustreasuryyieldcurve.com/ ; AOWM Calculations

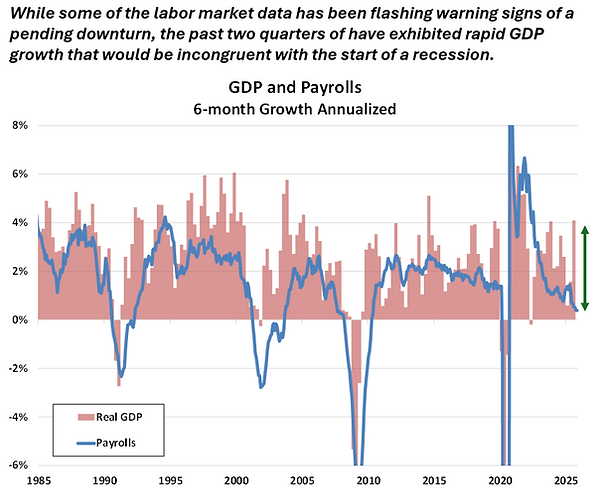

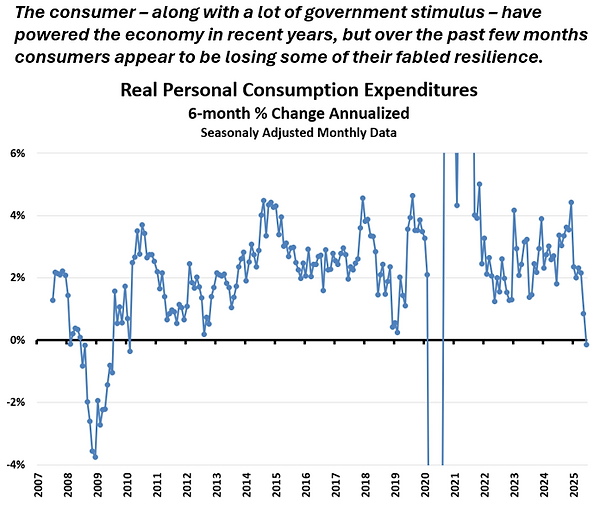

The Atlas Consumer | Still holding up the economy

December 29, 2025

The consumer continues to hold up the US economy with steady growth in spending. The US Department of Commerce estimated that Real GDP advanced at a rapid seasonally adjusted, annualized rate of 4.3% in the third quarter. While GDP growth has actually slowed over the past year, the fast growth of the past two quarters should allay recession fears fostered by the slowing labor market.

While a weak labor market could be the thing that makes the consumer pause, the risk of an imminent recession still seems low given the additional monetary and fiscal stimulus already in the pipeline for next year. The fundamental health of the economy over the long term, however, is more worrisome.

The growth in consumer spending has been dependent on a decreasingly small slice of the population and a general decline in the savings rate. At the same time, the federal government is running large deficits during a period of relative peace and prosperity. This lack of savings boosts current GDP and corporate profits, but at the risk of failing to make the investments necessary to keep the exponential growth machine going and handcuffing the government’s ability to respond to future crises. The economy’s margin for error is shrinking.

Source: YCharts ; fred.stlouisfed.org ; AOWM Calculations

Economic Data | Flowing again, even if still muddily

December 22, 2025

Government statistics for the labor market and consumer prices began flowing again last week after the shutdown interlude. On the surface, the inflation news was good and the jobs report worrisome. In reality, the opposite may be true.

Regarding the labor market, the unemployment rate has ticked up to a four-year high of 4.6% while payroll growth has stalled out in recent months. The trends in both are similar to what the economy experienced when slipping into recessions in 2001 and 2008. And yet other labor market statistics, such as claims for unemployment insurance, are not flashing the typical pre-downturn signals, offering some hope that perhaps the labor market is merely calibrating to the new normal of low population growth.

At the same time, the good news on consumer prices with headline CPI inflation falling to 2.7% is likely a statistical aberration because the shutdown prevented the usual collection of data. Such a swift decline in inflation would be more indicative of an economy in clear freefall than one just possibly sliding into a mild recession.

As has been the case since the pandemic, the data remains muddy with historical correlations decreasing in predictive value.

Source: YCharts ; fred.stlouisfed.org ; AOWM Calculations

The Fed | Becoming an AI believer

December 15, 2025

The Fed delivered the expected reduction in its target overnight interest rate last week, pushing short-term interest rates down to around 3.6%. Policymakers have now reduced rates by 1.75 percentage points since September 2024 even as inflation has remained above their 2% target, fiscal policy has remained highly stimulative, and asset valuations have continued to rise towards historical extremes.

In addition, the Fed announced it would resume growing its ample balance sheet which eliminates any pretense that monetary policy remains restrictive. The fed funds rate is still above policymakers’ median estimate of the neutral rate expected to prevail when the economy is at full strength and inflation is stable. However, after adjusting for still elevated inflation, the fed funds rate has more than likely already slipped back into stimulative territory.

In light of all the fiscal and monetary stimulus, it is reasonable that policymakers increased their forecasts for GDP growth next year. The Fed Chair also pointed to the continued strength of the consumer and ramping capital spending on AI as additional expected boosts to the economy in 2026. At the same time, policymakers less congruently reduced their expectations for inflation even while projecting an accelerating economy, banking at least in part on productivity gains aided by AI.

Our central bankers appear to be becoming AI believers just as investors are taking at least a momentary breather from the speculative frenzy. With the Fed's help, they may be back to partying before long.

Source: YCharts ; fred.stlouisfed.org ; AOWM Calculations

A Blind Cut | Insurance or accelerant?

December 8, 2025

The economic statistics that policymakers and investors rely on to guide their decisions are still not flowing as usual; nevertheless, the markets are priced for the Fed to blindly offer up another insurance rate cut this week. While headline inflation is higher now (or at least as of September) than it was when the Fed started lowering its target overnight interest rate in 2024, the markets and policymakers remain ever sanguine about the outlook for consumer prices.

There has been some growing weakness in the labor market which those pushing for lower rates view as justification for another rate cut. However, that apparent weakness may just be the new normal of minimal job growth due to aging demographics and low net migration, and more current private-sector data does not suggest a significant change in the labor market since the September jobs report.

Even if the economy is slowing, further monetary easing seems unnecessary given the fiscal stimulus in the pipeline and the strong wealth effect still emanating from the stock market.

Source: YCharts ; fred.stlouisfed.org ; https://trends.google.com/trends/ ; https://americanstaffing.net/research/asa-data-dashboard/asa-staffing-index/ ; https://www.chicagofed.org/research/data/chicago-fed-labor-market-indicators/forecast-details ; AOWM Calculations

Federal Budget | A runaway train

December 1, 2025

The federal government was shutdown in October but still managed to run a record deficit for the month. Even after adjusting for growth in the economy, the October deficit has been only exceeded in modern times by those that occurred during the great financial crisis or the pandemic.

Mandatory spending primarily on Social Security and Medicare and the growing cost of financing the federal debt drove the October deficit. Such predetermined spending has turned the federal budget into a runaway train that will not be easy to slow down.

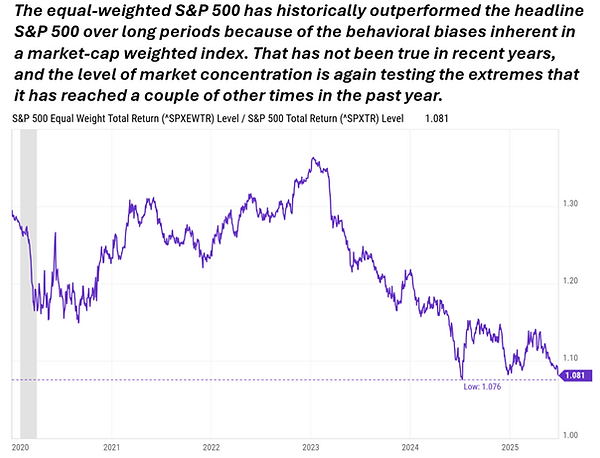

Meanwhile, the stock market ended November on an upswing with the S&P 500 chugging higher for the seventh straight month as investors cheered the growing signs that the Fed might reduce its target overnight interest rate again in December after all. However, despite continued good corporate profits and the prospects for even more government stimulus, the breadth of the current bull market continues to wane.

Source: YCharts ; fred.stlouisfed.org ; US Treasury ; https://www.cbo.gov/ ; https://www.spglobal.com/spdji/en/indices/equity/sp-500/#overview ; AOWM Calculations

Japan | Foreshocks or benign rumbles?

November 24, 2025

Japan’s economy contracted in the third quarter, and the new Prime Minister put forth an aggressive fiscal stimulus package to boost growth. The market response was not enthusiastic – Japanese stocks sold off, its long-term interest rates climbed higher, and the yen depreciated.

Ever more fiscal and monetary stimulus has been the playbook for policymakers over the past few decades and is likely to remain so until such policies unambiguously make things worse. At which point, there may be no easy escape from the excesses of the past. Where exactly the line lies between productive stimulus and a financial reckoning is unclear and is at least partly determined by the fickle psychology of the financial markets.

Given its high level of debt and extreme monetary policy, Japan has provided comfort for some time that other developed countries are far from trouble. But Japan may be a bad reference point with unique characteristics that have enabled it to stretch policy further than others can. Even if it is a good benchmark, a disturbance in the east could still quickly change the market’s permissive mood of recent years and move the line of reckoning for everyone else closer.

Source: YCharts ; fred.stlouisfed.org ; mof.go.jp/english ; AOWM Calculations

Euphoria's End | Always a half life away

November 17, 2025

The stock market is struggling to regain its upward momentum with declining expectations for another Fed rate cut in December playing at least some part. Yet more monetary and fiscal stimulus in the coming months could very well keep stocks rolling higher next year.

That a financial reckoning is on the horizon seems certain. But much like the highly anticipated recession in recent years that never arrived, perhaps valuations and profit margins will never mean revert. The already frothy markets are set to get a fresh boost of fiscal stimulus next year as the tax refund season should be a happy one for many, and the Supreme Court may force the Administration to throw in some unexpected tariff refunds as well. Meanwhile, the Fed, even if it doesn’t reduce rates in December, is still poised to reduce short-term rates further next year and resume growing its ample balance sheet.

All this government largess is wonderful until it isn’t. The end of the current euphoric market can only be put off forever in theory.

Source: YCharts ; fred.stlouisfed.org ; CBO.gov ; cmegroup.com ; Ray Dalio ; hussmanfunds.com ; AOWM Calculations

AI Bubble | What inning is it?

November 10, 2025

Last week, the behemoths sitting atop the stock market experienced some discombobulating selling pressure for the first time in months despite turning in generally good earnings reports. While optimism in the market remains high, the mild pullback may be indicative of some budding concerns that the hockey-stick projections for AI are not likely to be realized and that the hundreds of billions already spent will never generate good returns.

Some of the announcements for gigantic AI investments and complex interlocking deals amongst the major players are made with such opaqueness and audacity that they can’t help but generate skepticism. In addition, the markets have been weighed down in recent weeks by both the lengthy government shutdown that has deprived investors of the regular flow of economic data and the persistently dour economic outlook of many Americans.

Increasing levels of caution also seem reasonable in light of high valuations and a slowdown in the long-run uptrend in the market which suggest we are in the late innings of the current mania; however, excessive government stimulus and the wealth of the tech oligarchs could keep the game going into extra innings for the foreseeable future. At a minimum, the market is unlikely to commence a sustained downturn as long as corporate profits continue to march higher as they have so far this year. In an ideal world, stock prices would merely pause long enough to let the fundamentals catch up - there's a first time for everything.

Source: YCharts ; fred.stlouisfed.org ; topdowncharts.com ; www.spglobal.com/spdji/en/indices/equity/sp-500/#overview ; shillerdata.com ; data.sca.isr.umich.edu ; AOWM Calculations

The Fed | Slouching towards fiscal dominance

November 3, 2025

Policymakers at the Fed met last week and reduced their target overnight interest rate for the second meeting in a row. While Jay Powell, the Chair of the Fed, hedged a little on the prospects of another rate cut in December, the Fed did announce that it would stop shrinking its balance sheet next month, which should boost the amount of cash flowing through the financial system.

The stagnant labor market has provided policymakers with a fig leaf of cover to loosen monetary policy despite inflation trending higher, a seemingly resilient economy, euphoric financial markets, and excessive fiscal stimulus being pumped ceaselessly out of the nation’s capital. No self-respecting central banker would ever admit that the Fed is giving up the independence it won from the U.S. Treasury seventy-four years ago, but the writing does appear to be on the wall.

A grand bargain between the Fed and the Treasury where compliant monetary policy is pursued in conjunction with a prudent federal budget could be a good solution for the imbalances plaguing the economy. However, abdicating the Fed's independence without establishing a sustainable fiscal path forward is unlikely to solve anything.

Source: YCharts ; fred.stlouisfed.org ; www.atlantafed.org/cqer/research/gdpnow.aspx ; AOWM Calculations

Gold | Speculating on inevitable inflation and fear?

October 27, 2025

Despite a pullback last week, gold has been surging in value over the past three years, up nearly 150% while the doddering S&P 500 is up less than 80%. Gold is the quintessential fear trade that investors run to when the world appears to be falling apart, but the oldest financial asset is not immune to speculative fevers – they just don’t normally occur when the stock market is also melting up.

The fundamental underpinnings pushing gold higher are concerns about the systemic imbalances in the economy, an inflationary debasement of the dollar, and the de-dollarization of the world economy. General fear is also still likely playing a role – or at least narratives on how best to hedge the panic that seems inevitable to strike financial markets that are flying so close to the sun.

Gold is not only moving oddly relative to the stock market these days. For most of the past few decades, gold prices and the real yield on Treasury Inflation-Protected Securities (TIPS) moved in opposite directions, as gold is a more logical inflation hedge when real yields are low or negative than when TIPS offer a good real yield. That negative correlation has completely broken down over the past three years. TIPS with real long-term yields around 2% still appear to be the better - if less exciting - inflation hedge versus an asset with negative carrying cost and a spotty record of successfully hedging against inflation. However, if there is a complete breakdown in governmental institutions in the US, a shiny pet rock could be the emotional support animal we all need.

Source: YCharts ; fred.stlouisfed.org ; AOWM Calculations

Leverage | Every round goes higher, higher

October 20, 2025

Another year, another $2 trillion in borrowing by the federal government. Despite solid growth in tax receipts, new tariff revenue and efforts to curtail spending, the federal budget remained woefully out of balance in the 2025 fiscal year that ended on September 30.

The dysfunction that has kept the federal government shut so far this fiscal year does not bode well for the bi-partisanship needed to proactively address the nation’s fiscal imbalances. Whenever the next crisis inevitable comes, the powers-that-be will likely attempt again to flood the system with ever more borrowed (and/or printed) money, and it may yet work – or at least not result in catastrophe. But the results of the last attempt to do so warn that we may be reaching the top of the decades-long debt super cycle.

Even if the economy can lever up another leg higher without dire consequences, the extreme government stimulus is still fomenting trouble in the financial markets, which are busy levering up themselves in old and novel ways.

Source: YCharts ; fred.stlouisfed.org ; FINRA ; CBOE ; AOWM Calculations

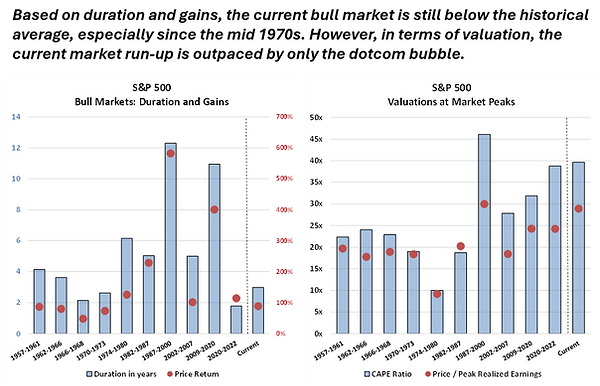

Bull Market | Turns three

October 13, 2025

The current bull market celebrated its third birthday with a bit of a tantrum on Friday. It was the first real bump in the road the market has experienced since the steep sell-off in April over tariff fears.

Having had only the smallest downtick to feast on in recent months, dip-buyers likely salivated all weekend at the chance to seize on the deals offered up by Friday’s decline. While this could be the beginning of the end of the market’s epic run, it is likely not the end just yet, so dip-buyers may still be rewarded for a while.

Compared to past bull markets – which are arbitrarily marked by periods following drawdowns of at least 20% – the current rally is still below average in terms of duration and gains; however, in terms of valuations, only the dotcom bubble surpasses it. The US stock market has arguably been in one long cyclical bull market since 2009, much like the run in the market from the early 1980s to the peak in 2000.

Comparisons to the late 1990s are ubiquitous these days. While the technology is potentially even more transformational this time around, the macroeconomic background is definitively less healthy, making walking on air even more risky.

Source: YCharts ; fred.stlouisfed.org ; www.dallasfed.org/research/economics/2025/1009 ; AOWM Calculations

Investor Sentiment | Too hot? (same question as last October)

October 6, 2025

Investor enthusiasm is best in moderation; however, like many things, little time is spent at the golden mean. The market’s animal spirits are more often running from one extreme to the next. Since the bottom of the great financial crisis in 2009, investors have been growing steadily more confident and carefree with the few brief hiccups experienced only serving to strengthen their resolve to buy every dip.

In an ideal scenario: the market is running slightly above its long-run moving averages which are trending nicely higher (but not too quickly); earnings expectations are trending higher optimistically (but not overly so); valuations are reasonable (or better yet cheap); no one theme is monopolizing the market narrative; equity allocations are near historical averages (or below but trending back up); margin debt is growing slowly; and options activity is not noteworthy. These days investor sentiment is running impatiently away from the ideal.

Accordingly, stocks kept churning higher last week despite a government shutdown (or perhaps in part because of it as the shutdown also stopped the release of any government data that might disrupt the current bullish zeitgeist). But the shutdown won’t stop the upcoming release of quarterly corporate earnings for which expectations have been rising.

Source: YCharts ; fred.stlouisfed.org ; S&P Global, AOWM Calculations

Spending | Even more resilient than prior estimates

September 29, 2025

Economic growth in the second quarter was revised higher again driven by stronger consumer spending than initially estimated. The annual update to the GDP data going back five years also revised up estimates for personal consumption over the past two years.

Through the first half of the year, it had appeared that the consumer was starting to slow down, but the revisions and monthly data through August suggests that is not the case – which remains at odds with the low level of consumer sentiment. The survey data may be partly explained by only the top of the income ladder really enjoying much growth in real spending.

Much like the concentrated stock market, the narrow strength of the economy makes it more fragile. Nevertheless, the flywheel spins on and is still expected - despite its resilient speed - to get an extra push from the Fed in the coming months.

Source: YCharts ; fred.stlouisfed.org ; Moody's Analytics ; Morning Consult ; BEA ; AOWM Calculations

Rate Cuts | Not the textbook response

September 22, 2025

The financial markets are exhibiting speculative froth; inflation is trending higher; unemployment remains low; policymakers are raising their forecasts for inflation and GDP growth; and the Fed just cut its target overnight interest rate and indicated more reductions are likely in the coming months. That is not the textbook policy response to the delineated economic conditions.

Nevertheless, investors are expecting even more unorthodox rate reductions than projected. Policymakers’ median forecast is for the fed funds rate to fall to 3.4% next year while the market is priced for short-term rates to decline below 3%.

Given the stock market’s positive response to the Fed’s latest policy announcement, the expectation for greater rate cuts does not appear to be driven by a fear of recession – which would be a more textbook rationale for lowering rates. Meanwhile, in the bond market, long-term interest rates ticked higher last week, also indicative of minimal recession concerns (but potentially some lingering inflation worries).

If the economy remains generally healthy and the federal deficit robust, the level of monetary easing projected by either policymakers or investors could prove to be counterproductive.

Source: YCharts ; fred.stlouisfed.org ; Moody's Analytics ; AOWM Calculations

The Fed | A predictable future?

September 15, 2025

The latest CPI report showed inflation continuing to trend in the wrong direction; nevertheless, the financial markets are fully priced for the Fed to begin cutting its target overnight interest rate again this week. Not doing so would be truly surprising, and central bankers these days dread being surprising even more than being wrong.

While stock valuations remain stretched at historically high levels, additional monetary easing could supply the fuel necessary to keep the upward momentum going - a potentially self-fulfilling belief at least in the short run. Meanwhile in the bond market, a general anticipation that the Fed will ultimately be fully co-opted to assist with financing the federal debt may be keeping long-run Treasury rates in check despite a deficit that seems untamable.

Both are reasonable expectations; however, it is wise not to place too much faith in our predictive powers.

Source: YCharts ; fred.stlouisfed.org ; AOWM Calculations

Jobs Report | Newsworthy repetition

September 8, 2025

The latest jobs report was newsworthy, but the story it told was much the same as it has been telling for over a year. The market swung up and then down on the newsworthy part, first cheering the prospects of the report prompting the Fed to lower rates more aggressively and then worrying about why the Fed might need to cut rates more aggressively.

On the newsworthy side, revisions to the payroll data indicated that payrolls actually declined in June for the first time since 2020 and the unemployment rate ticked up in August to 4.3% - the highest since October 2021. And yet the report mainly repeated the longstanding narrative of an unusually stagnant private labor market that is neither shrinking nor really growing – which given the nation’s increasingly stagnant population is all that has been necessary to keep the labor market largely in balance.

Investors continue to anticipate a goldilocks scenario where the labor market continues to weaken sufficiently to encourage the Fed to lower rates but doesn’t suffer a significant downturn. That outlook largely ignores how policymakers may be constrained from cutting rates by high inflation – or the potential ramifications of failing to be so constrained.

Source: YCharts ; fred.stlouisfed.org ; topdowncharts.com ; www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html ; AOWM Calculations

Corporate Profits | No worries, but for the k-shape

September 1, 2025

At the national level, corporate profitability remained strong in the second quarter showing no signs indicative of an economy in or near a recession. However, much like with the consumer, the wealthiest companies have been thriving while the rest have not.

Corporate profits soared across the board after the pandemic on the back of massive government stimulus. Since then, most of the gains have gone to the biggest companies -- which has been the fundamental basis for the increasing concentration of the stock market over the past few years.

The current hope is that lower interest rates and a more friendly regulatory environment will enable more companies to boost earnings as the largest see their torrid growth slow to a merely robust mid-teens rate. A broadening of corporate profit growth would provide a firmer foundation for the economy and the market.

Source: YCharts ; fred.stlouisfed.org ; www.spglobal.com/spdji/en/indices/equity/sp-500/#overview ; AOWM Calculations

Lower Rates | Then what?

August 25, 2025

The Fed Chair gave a speech on Friday, and the financial markets cheered the prospect of lower interest rates. Time will tell. Investors have repeatedly anticipated rate cuts that have failed to materialize, and economic data over the next month could change the outlook yet again. Even if the Fed does lower its target overnight rate a bit more, it is far from clear in this up-is-down world how stimulating that really would be for the economy.

First, asset valuations are already “notable” (to use the Fed’s own term in its latest assessment of financial stability). So while further easing risks making things more unstable, further upside stimulus through the wealth effect is limited.

Second, lower short-term rates do not guarantee that long-term rates will follow. Since the Fed first cut rates last September, long-term Treasury, corporate and mortgage rates are all higher.

Third, higher interest rates have yet to hinder corporate America significantly as companies had loaded up on ultra-low-rate debt during the pandemic, which is only slowly being refinanced at higher rates. That normalization process will continue to be a headwind for companies in the coming years unless the Fed takes monetary policy back to extreme levels with zero percent rates and a large expansion of its balance sheet.

Lastly, this is the first significant tightening and loosening cycle of monetary policy with the Fed paying interest on oversized liabilities - which makes the Fed’s rate moves less countercyclical as the Fed injects billions into the financial system via interest payments as rates go up and conversely reduces that stimulus as rates come down. Similarly, lower short-term rates would also slightly bring down the interest expense on the national debt and the federal deficit, mildly reducing that generous stimulative boost to consumer spending and corporate profits.

Given all we have seen in recent years, it is hard to see how anyone is confident about what comes next.

Source: YCharts ; fred.stlouisfed.org ; federalreserve.gov ; econforecasting.com/forecast/ffr ; AOWM Calculations

Central Bankers | Anchored to easy money

August 18, 2025

Inflation continues to complicate the desire for lower interest rates. CPI inflation crept higher in July while the Producer Price Index spiked significantly higher than expected. Nevertheless, the market remains fully priced for the Fed to resume cutting its target overnight interest rate in September.

Fed policymakers profess a dual mandate to “achieve maximum employment and inflation at the rate of 2 percent over the longer run.” Putting aside quibbles about the Fed’s actual statutory mandate and what monetary policy can achieve, the status of the economy relative to those two stated goals alone is at odds with the expectation for an imminent easing of policy. The unemployment rate remains low at 4.2% in line with estimates for full employment (assuming an inherent level of frictional unemployment in the economy) while inflation remains stubbornly above the Fed’s definition of “stable prices” as it has for more than four years.

However, the crises and conditions of the past few decades have ingrained a bias towards loose monetary policy – which a slowing economy, weakening labor market and burgeoning national debt only make more challenging for policymakers to overcome.

Source: YCharts ; fred.stlouisfed.org ; AOWM Calculations

Stocks | Stretching the imagination

August 11, 2025

The S&P 500 finished last week a tick below its all-time high while the Nasdaq continues to march steadily higher into uncharted territory. By almost all metrics, the valuations of US large cap stocks have outpaced the fundamentals. And by some metrics, the US stock market has never been so richly valued or so concentrated as it is today.

Such manic moments stretch the imagination for how wild they can get. When Microsoft’s valuation topped out around 6% of GDP at the peak of the dotcom bubble in 2000, one might have imagined that was a reasonable benchmark for an extreme valuation (especially after it fell back to less than 1% of GDP in 2009). But Microsoft – the one company to enjoy both the heights of the dotcom and pandemic/AI bubbles – blew past that quaint 6% marker in 2020; and then it appeared 10% in 2021 might be the new peak; and then almost 12% last year; however, after the recent run-up from the April low, Microsoft is now valued at around 13% of GDP -- and some assert we’re just getting this speculative frenzy warmed up.

Who’s to say where this stops? But if the dotcom bubble is any guide, the end can be abrupt with today’s insatiable appetite quickly becoming tomorrow’s regrettable stomachache.

Source: YCharts ; fred.stlouisfed.org ; Augur Infinity ; AOWM Calculations

Economic News | Summer deluge

August 4, 2025

In the dead of summer last week, there was a deluge of economic news. In addition to the ongoing back and forth over tariffs, there was a bevy of earnings reports including four of the so called “Magnificent Seven” mega-cap stocks; the latest GDP numbers were released along with reports on the Fed’s preferred PCE inflation metric and the labor market; and policymakers at the Fed announced their latest decision to keep the fed funds rate unchanged. On net, the news gave investors pause as the stock market gave back some of its recent gains and long-term interest rates declined.

With respect to the economy, growth slowed further in the second quarter as consumer spending has stalled over the first half of the year. Estimates of job growth also continued to decelerate driven in large part by a downward revision in government jobs, but the unemployment rate remained relatively low at 4.2% given the changing demographics of the country requiring fewer jobs to maintain full employment. At the same time, PCE inflation picked up in July and continued to trend away from the Fed’s 2% target.

Policymakers and investors could be facing the odd mix of an economic downturn, low unemployment, and high inflation. Given the frothy state of asset prices, the steady growth of the money supply, and the Fed’s mandate to focus on employment and inflation (not GDP growth), the case for further rate cuts is weak. However, additional cuts are likely before year end. And yet, it is dubious that further monetary easing will give the economy enough of a boost to achieve investors’ lofty earnings expectations which remain incongruent with slowing GDP growth.

Source: YCharts ; fred.stlouisfed.org ; BLS ; BEA ; AOWM Calculations

AI | Necessarily disruptive

July 28, 2025

If it feels like the pace of change is accelerating, that is because it is. We are reaching the second half of the proverbial chessboard where exponential growth can be particularly discombobulating and hard to fathom. Advances that were once experienced over a lifetime just a generation ago now zoom by in a matter of years or seemingly months.

Perpetual growth is taken for granted (especially in current asset valuations); however, it has required repeated technological discoveries to overcome past constraints. The compounding of human knowledge, of which AI is the latest and potentially ultimate culmination, has thus far enabled humanity to leap over every hurdle. The increasing challenge is that as things move faster and faster, the hurdles come at us faster as well, and the pain of a potential tumble also grows.

Despite the increasing speed, the margins for safety have been worn perilously thin with high asset valuations, elevated leverage, and low levels of societal trust. AI’s biggest hurdle to keeping the world growing may not be finite resources but humanity’s hubris.

Source: YCharts ; fred.stlouisfed.org ; www.eia.gov ; www.energy.gov ; JP Morgan ; Scale by Geoffrey West ; United Nations ; AOWM Calculations

Inflation | Why worry?

July 21, 2025

After three months of relatively benign inflation reports, CPI inflation reaccelerated in June, and the consensus forecast is that tariffs will keep inflation trending further away from the Fed’s 2% target in the coming months. Despite rising inflation and increasing inflation expectations in the TIPS market, investors still expect the Fed will reduce its target overnight interest rate by half a percentage point before the end of the year.

There is a growing chorus of pressure for the Fed to move sooner rather than later with the expectation that any tariff-induced inflation will be transitory. More traditional voices advocating for looser monetary policy believe the economy is weakening quickly and in need of lower rates to avoid a recession. Others assert that the coming AI revolution is going to be so deflationary with unprecedented supply-side growth that the Fed doesn’t need to worry about inflation.

In addition, the president has been blunt in his desire for the Fed to help lower the interest expense of the federal debt. The pressure campaign from the president suggests the independence of the Fed may be on borrowed time – which would be a logical reason to worry about inflation if it is not simultaneously coordinated with a significant reduction in the federal deficit.

Source: YCharts ; fred.stlouisfed.org ; fiscaldata.treasury.gov/datasets/monthly-statement-public-debt/summary-of-treasury-securities-outstanding ; AOWM Calculations

AI Fever | It's summertime

July 14, 2025

Last week, Nvidia became the first company to reach a $4 trillion market valuation. It is becoming a summer tradition for Nvidia to celebrate such milestones as it cracked the $1 trillion level in June 2023 and the $3 trillion level in June 2024. It has been an astonishing run for the business and even more so for the stock. It is fitting that one of the biggest FOMO trades of all time has a name derived from the Latin word for envy.

Is it too late to join the party? It seems unlikely Nvidia will be hitting $5 or $6 trillion next summer, but it was hard to imagine it reaching this level, even just a few months ago after it had swiftly lost 35% of its value to start the year. Policymakers could help to keep the music playing for a while. If the Fed lowers rates later this year when the market is still running hot, momentum could carry things to more extreme levels.

However, even if AI is as magical as its biggest proponents assert, Nvidia has reached a valuation where both economic and political headwinds will depress long-run returns. Is Nvidia likely to grow (or be allowed to grow) to be worth more than 20% of GDP a decade from now – which is what a 10% annualized return from here would likely imply? Is it likely to even still be worth the more than 13% of GDP that it is now? History would suggest not.

As indicated by its extreme volatility, Nvidia has been more a trade than a buy-and-hold stock for some time. So far shareholders have only been really rewarded if they have been brave (foolish?) enough to sell. When to get off such a speculative juggernaut is the hardest part for those fortunate enough to be on it and is fraught with as much potential regret as those who never bought the stock.

Source: YCharts ; AOWM Calculations

The Government | Sails at full speed

July 7, 2025